2025 has been a bit of a wild ride in terms of investment markets, to say the least, with just about every region and asset class across the globe experiencing significant volatility at some point this year.

While markets were already a little unsettled prior to ‘Liberation Day’, the US imposition of tariffs on most trading partners has sent shockwaves through markets. Companies who have become very used to relatively frictionless trade and wide access to the biggest* consumer market are now struggling to do business as their supply chains face significant challenges.

Below, let’s explore how financial advisers can deal with market downturns, how we learn from the ‘lost decade’ and why currency diversification can be a crucial element of true diversification.

Avoiding reactivity

First of all, the most important thing is not to be reactive to markets (and re-iterate to clients that reacting to market downturns and selling assets in a falling market is one of the worst things you can do for long term growth – it’s time in the market, and not timing the market after all!). The next most important thing, in my opinion, is a diversified investment strategy.

Concentration risk is very real and hopefully this year so far has been a bit of a wake-up call for those who needed it (he types, putting his own hand up!).

Over the last few years, many investment providers have allocated a significant amount to US equities either directly (as a result of active investment choices to benefit from the strong returns) or inadvertently (pure passive strategies where the exceptional growth of US companies, relative to the rest of the world, naturally led to a skew to the US in market-cap weighted underlying indices).

Learning from the lost decade

Ignoring the year so far, it’s easy to see why many active managers will have done so as the growth in US equities has been impossible to ignore. But, has the US always been this favourable?

There was a time (termed ‘The Lost Decade’) when US equities were relatively unattractive to investors, which is difficult to believe in this day and age. Between 2001 and 2011, the US market was ‘underwater’, meaning that if you invested money in the US equity sector in early 2001, then you would not have seen a positive return on your investment until December 2011.

As you can see on the chart below, prepared by IBOSS as part of our joint webinar, the US equity sector even underperformed global equities as a whole. Over the same timeframe, buying into emerging market equities – which are today sidelined in the majority of portfolios, returned over 300%.

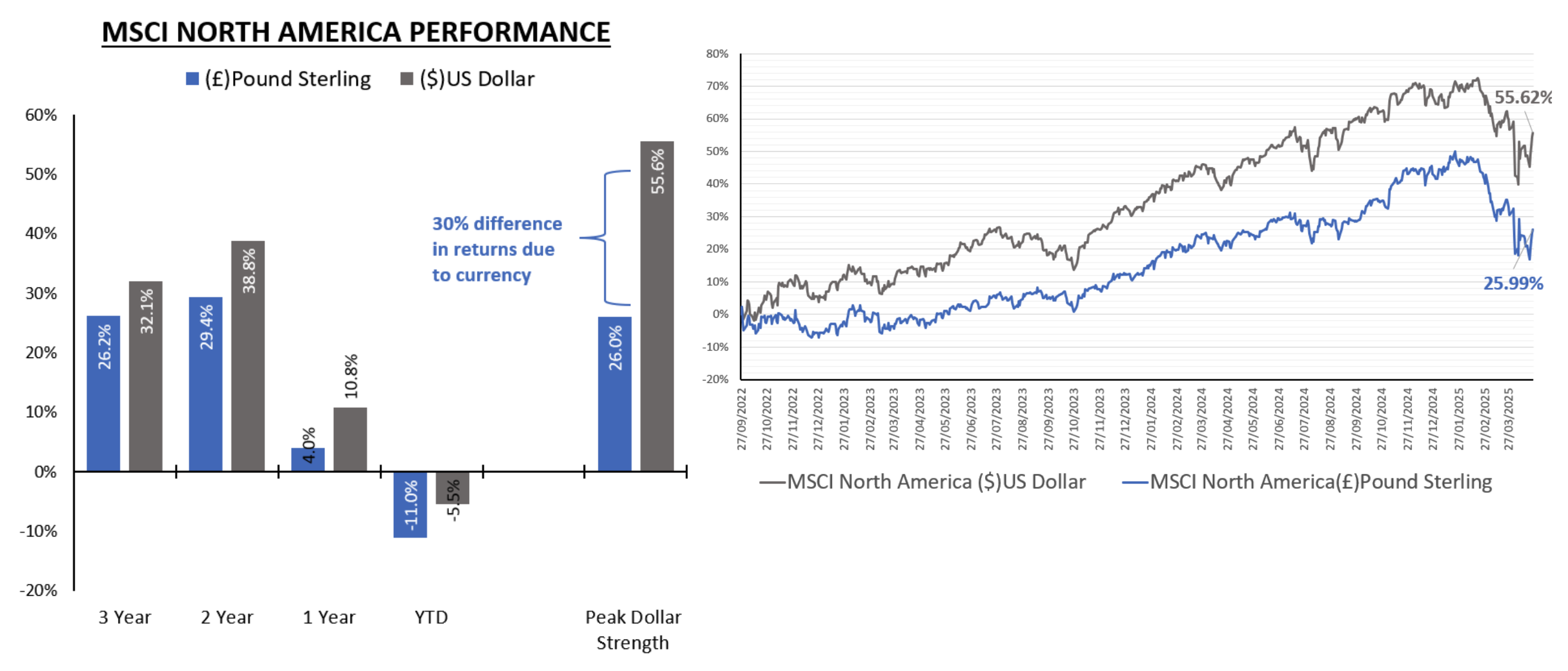

Currency Diversification

Diversification can not only be brought about via investing in different markets (and different asset classes), but one often overlooked consideration is that of currency. Currency can also have a material impact on returns, both positively and negatively depending on where you are investing vs where you will be spending.

The charts above highlight just how much of an effect currency can have when it comes to investment performance. Looking back over the last few years, investors with holdings denominated in US Dollars would have seen a significant advantage in terms of returns compared to those with holdings denominated in Pounds Sterling. Could we see a reversal in this trend over the next few years?

Again as with any investment decision, it’s best practice not to speculate but rather have a broad exposure to key, stable currencies across the globe. Many MPS providers will denominate select funds in their portfolios in different currencies to achieve some level of currency diversification, but it’s best to check that it’s part of their process as part of your own due diligence.

To wrap up, nobody knows for sure what the next decade will look like in terms of which asset class, currency or geographical market will perform the strongest relative to the rest of the world, particularly given what’s happened over the last 6 months and the huge shift in favour from the US to …. who knows?

At the moment, we seem to be paused at a major crossroads while the world re-organises itself in terms of trade and relationships between countries.

The best we can do right now is to ensure a broad spread of asset types, market geographies and currencies that will help place an investment strategy in the best position to capture the next ‘big thing’ before we even know what it is yet.

Grant is a financial planning specialist at Verve, with broad experience offering technical support and creative solutions to improve advice firms' operations.

.png)

.png)

.png)